|

PRESS Release April 28, 2014 |

|

YOUSHOJI, Ltd |

YOUSHOJI, Ltd. Japan: A Business Method of Accounting under Standard Costing, Unifying Management and Financial Accounting, was Admitted as a Patent by the USPTO (2013)

Hayashi, Yuichiro, Dr. Eng., President of YOUSHOJI, Ltd., Japan is

proud to announce the issuance of the US patent, entitled “Accounting method

and accounting system", No. US 8,554,646 B2, Oct. 8, 2013. The patented method of accounting under standard costing

utilizes a new break-even chart which unifies management accounting and

financial accounting under standard costing.

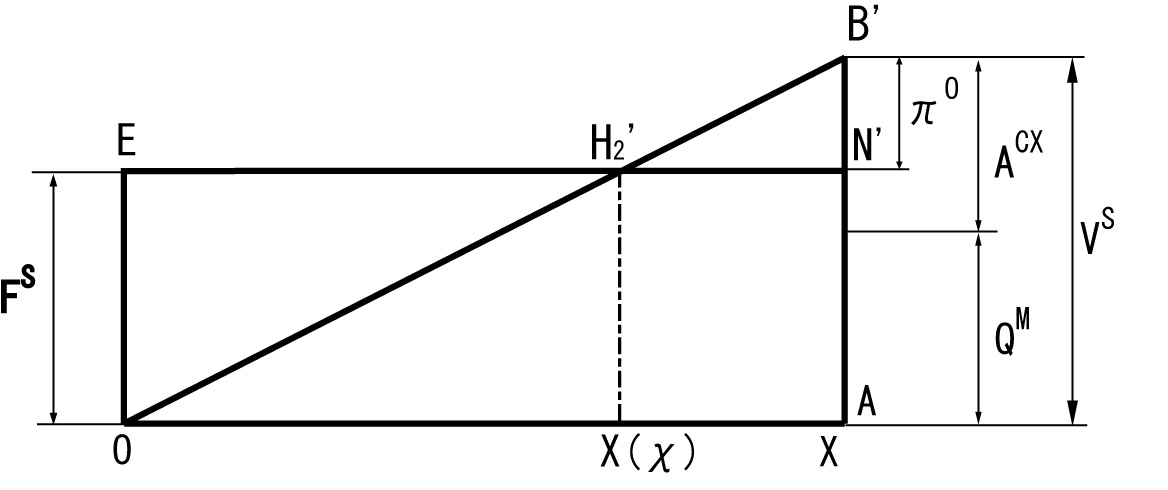

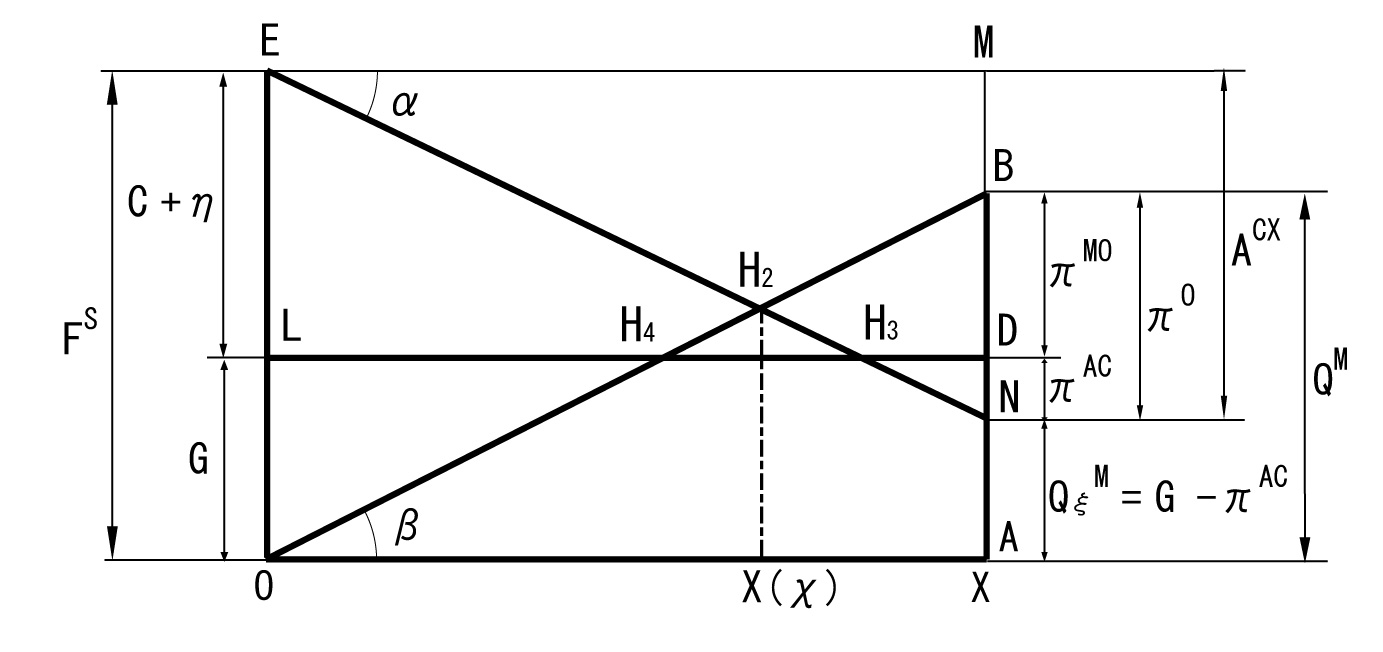

■ 2013 Profit Chart and 2007 Profit Chart under Standard Costing

The break-even chart under standard costing (hereinafter referred to

as a profit chart) used in the US Patent in 2013 is shown in Figure 1 (2013 Profit

Chart). Figure 1 is closely associated with the US patent entitled “Accounting system for absorption costing”,

NO. US 7,302,409 B2, Nov. 27, 2007. The profit chart used in the US patent in

2007 is shown in Figure 2 (2007 Profit

Chart).

Figure

1. 2013

Profit Chart

Figure2. 2007 Profit Chart

■ Operating Profit under Standard

Costing

In

standard costing, we determine the operating profit at the end of the final

year as the result of the following process. Let X be “Sales or Goods sold”; Q

be “Sales gross profit”; πO

be “Sales operating profit”; DX be

“Manufacturing direct cost (variable and actual) ”; C be “ Manufacturing overhead cost (fixed and actual) ”; G be “Selling and administrative costs

(fixed and actual) ”; E be “ Manufacturing

absorption cost”; ACX be “Manufacturing

overhead allocation cost to X”; ACY

be “Allocation revenue of C accounting department during the present

accounting period”; ACY( + )

be “Year-ending ACY carried forward to inventories”; ACX(

- ) be “Year-beginning ACX carried down to X”. η (eta) = ACX(-) - ACY(+)

= ACX - ACY is named “Net carryover manufacturing

overhead allocation cost”. Operating profit πO is obtained as

follows. : Q = X – E; E = DX + C + ACX( - ) - ACY( +

) = DX + [C + η]; πO = Q – G = X - DX -

[C + η + G]

·····(1). Eq. (1) shows that the amount of η affects the value of πO.

■ 2007 Profit Chart

For

management accounting under standard costing, besides the above-mentioned

notations, we define the following accounting technical terms and notations at

any given point in time during a year accounting period, e.g. a monthly or even

weekly ending. Let EM = DX

+ ACX be “Managed manufacturing absorption cost”; QM = X - EM be “Managed

gross profit”; πMO =

QM - G be “Managed operating profit”; πAC = ACX - (C + η) be “Managed allocation

profit” or “Managed manufacturing overhead allocation profit”; δ =

ACY - C be “Manufacturing overhead variance”; VS = X - DX be “Marginal profit”; FS = C + η + G be

“Managed fixed cost”. Using those notations, we obtain Figure 2 expressing the

locus of the marginal condition where πO =

0 is satisfied in Eq. (1). Observing Figure 2 gives πO

= πMO + πAC and πAC = ACX - (C +

η).

Since η = ACX

-

ACY,

we can also express πAC = δ.

Since none of the formal terms had existed in conventional accounting, the

inventor coined these for management accounting.

■ 2013 Profit Chart

The inventor was stressing to the employees that managed fixed

cost FS including η shown in Fig.2 is a constant. However, the

marginal gross profit ratio line (segment EN), which should connect with FS

is an oblique line from top left to bottom right. Since such a profit chart has

not been taught in accounting education, the more educated members in

accounting feel disinclined to use the 2007 Profit Chart. Therefore, the

inventor began to research how to draw the line FS horizontally in Figure

2. As a result, the inventor created the 2013 Profit Chart shown in Figure 1 by

transforming Figure 2 into Figure 1. We can easily transform Figure 1 into a 45 degree break-even chart, which is

equivalent to Eq. (1). In

Figure 1, if we let η = 0 and ACX = 0, we can obtain

the profit chart or the marginal profit chart, under direct costing, where FD

=

C + G

is expressed as a horizontal line. Consequently,

since both Figure 1 and Figure 2 are equivalent to each other, they include the

direct costing profit chart.

■ Significance of the Patent

It is very useful for a company to use this accounting method in

order to manufacture a wide variety of products where each product’s accounting

is treated as a profit center. The

outstanding problem for many decades concerning the difference between standard

costing and direct costing profit charts is now solved. This means that both

standard costing and direct costing are unified.

■ More Information

The 2007 Patent and the 2013 Patent are easily searchable on

Google Patent. More Information is available on the inventor’s website. URL:http://www11.plala.or.jp/yuichiro-h/. The website

can

also be accessed by searching for “Making-Digesting-Burning”. Additional

information on the website includes an overview and the inventor’s resume.

■ Contacts

YOUSHOJI,

Ltd.

4-29,

Hamada 1-chome, Sakata-shi, Yamagata, 〒998-0031,

Japan

President

Hayashi, Yuichiro

tel.

+81-(0)234-23-22

E-mail: yuhayashi@ymail.plala.or.jp

|

|

|